A Swiss gold bar is one refined in Switzerland by Argor-Heraeus, Valcambi, PAMP, or Metalor. These four — three in Ticino, one in Neuchâtel — hold LBMA Good Delivery accreditation for gold and operate under the Swiss federal precious-metals control regime. Between them they refine a substantial share of the world’s newly produced gold each year. Each has its own owner, its own history, and its own focus inside the bullion market: Argor-Heraeus runs as the Swiss arm of Heraeus Precious Metals, the Hanau-based German group whose industrial precious-metals operations are among the largest in Europe; Valcambi is owned by India’s Rajesh Exports and built around very large single-site capacity; PAMP, part of the Geneva-based MKS PAMP Group, is the most recognised name in branded minted bars; Metalor, owned by Japan’s Tanaka Kikinzoku Kogyo, refines gold alongside a wider industrial precious-metals business. The refiner behind a given bar determines which mark it carries, in which formats it was produced, and how readily it resells.

What “Swiss gold bar” denotes

Switzerland has no commercial gold mining domestically. “Swiss” in the bullion context describes where a bar was refined and cast or minted, not where the metal came out of the ground. The source material is mining doré from anywhere in the world, recycled gold, or wholesale gold from other refiners. What the Swiss origin marker certifies is the refining and bar-forming step — done by a refiner accredited to the Good Delivery standard and operating under the Swiss federal precious-metals control regime.

Two regulatory layers apply at once. LBMA Good Delivery, administered by the London Bullion Market Association, accredits refiners on assay accuracy, financial standing, and supply-chain due diligence; bars produced to the Good Delivery specification by an accredited refiner are deliverable into the wholesale market. The Swiss federal regime — the Precious Metals Control Act and its implementing ordinance, administered by the Federal Bureau for Precious Metals Control — governs hallmark, assay, import/export, and trade-license requirements within Swiss territory. The two regimes do different work: LBMA accredits the refiner; Swiss federal precious-metals control governs the metal itself once it is in or moving through Swiss territory.

Specifying Swiss origin in a contract carries three practical effects at once. Between them, the four refiners produce a substantial share of Good Delivery gold each year, which makes “Swiss” effectively shorthand for “available at scale.” Argor-Heraeus, Valcambi, PAMP, and Metalor sit among the most universally accepted refiner marks in the secondary market — a Swiss-marked bar resells through institutional counterparties without dispute over the refiner’s authority. And across the four, a buyer can source 400 oz cast bars, cast or minted kilobars, sub-kilo branded formats, and segmentable products from a single regulatory perimeter.

The four LBMA-accredited Swiss gold refiners

Three of the four — Argor-Heraeus, Valcambi, PAMP — operate in Ticino, the Italian-speaking canton in the south, within roughly thirty kilometres of one another. The fourth, Metalor, sits in Neuchâtel in the French-speaking west. Ownership today spans Germany, India, Switzerland, and Japan; founding dates span more than a century; product orientations cover the full range of gold-bar formats, from wholesale Good Delivery refining to design-recognised retail-investment minting.

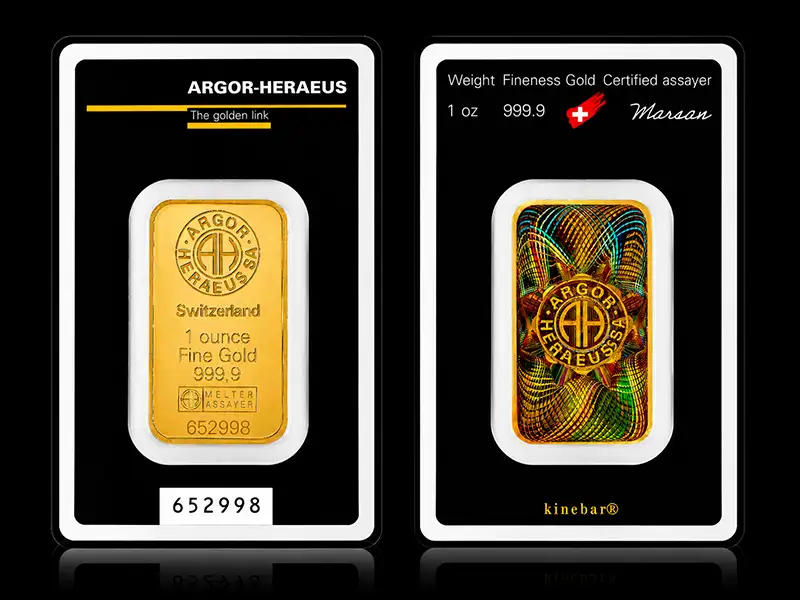

Argor-Heraeus SA — Mendrisio, Ticino

Heraeus Precious Metals, the Hanau-based parent group, runs one of the largest industrial precious-metals operations in the world. The group was founded in 1851 by Wilhelm Carl Heraeus and now spans automotive-catalyst recycling, semiconductor PM materials, dental and medical alloys, fibre optics, and electroplating chemistry — refining, recycling, and PGM trading sit alongside that wider industrial footprint, and the global supply network and central-bank reach behind the group’s bullion arm rest on it.

Argor-Heraeus is the Swiss-based gold and silver refining operation within that business. Founded as Argor in Ticino in 1951, it expanded under Heraeus’s investment, became Argor-Heraeus, and now operates as a wholly owned Heraeus subsidiary after the parent consolidated full ownership in 2017. The Mendrisio site holds Good Delivery accreditation for gold and silver and LPPM Good Delivery for platinum and palladium. The product range includes:

- 400 oz Good Delivery cast bars

- Cast and minted kilobars

- Branded minted bars across the institutional sub-kilo range — 1 g, 5 g, 10 g, 20 g, 50 g, 100 g, 250 g, 500 g, and 1 oz

- Coin blanks and coins struck for sovereign and private mints

- Semi-finished products and precious-metals grain

- The proprietary KineBar — a minted bar with an embedded kinegram security feature, available in 1 g, 5 g, 10 g, 20 g, 50 g, and 100 g formats

- “100% Hydropower” line and mine-traced provenance-certified products under Argor-Heraeus’s traceability programs

Among the Swiss four, Argor-Heraeus is distinct in being embedded inside a larger industrial precious-metals group rather than operating as a refining-led standalone. For an institutional buyer that translates into supply continuity across cycles, technology and assay capability inherited from the parent, and access to the Heraeus network of central-bank and bullion-bank counterparties through the same entity.

Valcambi SA — Balerna, Ticino

Balerna sits roughly thirty kilometres south of Mendrisio in lower Ticino, and the Valcambi facility there operates on the highest single-site refining capacity among the Swiss four. Public reporting cites annual gold refining capacity above 2,000 metric tonnes, with substantial silver and PGM throughput in addition — a scale built around a high-volume wholesale model rather than a multi-site network, which concentrates technical and assay capability in one place.

The history runs through the Swiss banking system. Founded in 1961, Valcambi developed under Credit Suisse ownership through the second half of the twentieth century and grew alongside the bullion flows the bank-led Swiss precious-metals business carried in those decades. Credit Suisse exited the refining business in 2003, divesting its stake to a consortium led by Newmont Mining and Valcambi management. Rajesh Exports Limited, a Bangalore-listed Indian gold and jewellery group, acquired the majority stake in 2015 and remains the owner today.

Balerna holds Good Delivery accreditation for gold and silver and LPPM Good Delivery for platinum and palladium. The product range includes:

- 400 oz Good Delivery cast bars

- Cast and minted kilobars

- Sub-kilo and gram-scale branded minted bars

- Coin blanks supplied to sovereign and private mints

- Semi-finished products and precious-metals grain

- The proprietary CombiBar — a segmentable bar introduced in 2011, available in gold, silver, and platinum, with the gold formats most commonly built as sheets of 50 × 1 g and 100 × 1 g that snap into individual one-gram pieces

Two operational features stand out. High-throughput Good Delivery output supports buyers placing very large institutional volumes where supply availability matters more than format detail. And product innovation in segmentable retail-investment format — the CombiBar specifically — gives Valcambi a position in the secondary market that the other three Swiss refiners do not occupy.

PAMP SA — Castel San Pietro, Ticino

PAMP is the most recognised name in branded minted gold bars. The Lady Fortuna design — introduced in 1979 as the first decorated minted bar in modern bullion — established that branded position early and has remained in continuous production since, with PAMP-marked minted bars carrying some of the strongest resale recognition in the retail-investment segment globally.

The full name is Produits Artistiques Métaux Précieux, founded in Castel San Pietro in 1977. The refining and minting operation sits within the MKS PAMP Group, an integrated bullion business whose corporate parent is MKS (Switzerland) SA — a Geneva-headquartered precious-metals trading group with operations across trading, refining, vaulting, fabrication, and technology. PAMP holds Good Delivery accreditation for gold and silver.

The product line is the broadest among the Swiss four on the branded side:

- 400 oz Good Delivery cast bars

- Cast and minted kilobars

- Sub-kilo minted bars across the full range — 1 g, 2.5 g, 5 g, 10 g, 20 g, 1 oz, 50 g, 100 g, 250 g, 500 g

- Design-recognised series: the Lady Fortuna bar, the Rosa series, and the FIDES proof line

- Coins struck for sovereign and private mints, plus blanks

- Recycled-source and mine-traced gold lines under PAMP’s traceability and provenance programs

On the wholesale side PAMP runs the full Good Delivery refining capability typical of the Swiss four; what distinguishes the operation commercially is the depth of the branded minted-product line, the trading reach of the MKS group around it, and the secondary-market liquidity PAMP-marked product carries through brand recognition built over more than four decades.

Metalor Technologies SA — Neuchâtel

Metalor’s Neuchâtel facility traces back to 1852, making it the oldest operation among the Swiss four and one of the longest continuous precious-metals refining sites in Europe. The business operated under the Métaux Précieux SA name through much of the twentieth century before reorganising as Metalor Technologies SA in its modern form. Tanaka Kikinzoku Kogyo, the largest precious-metals group in Japan, acquired Metalor in 2016 and remains the owner today.

The business itself is broader than bullion. Metalor’s portfolio at group level spans electroplating chemistry, dental alloys, electrotechnical components, advanced surface coatings, advanced materials for the electronics and medical-device industries, and assay and refining services for industrial customers — refining is one of several business lines within an industrial precious-metals operation, and the Swiss bullion supply discussed here originates specifically from the Neuchâtel facility (Metalor also operates in the United States, Singapore, Hong Kong, France, and elsewhere).

On the bullion side, Metalor holds Good Delivery accreditation for gold and silver and LPPM Good Delivery for platinum and palladium. The Neuchâtel output covers 400 oz Good Delivery cast bars, kilobars in cast form alongside selected minted formats, branded minted bars at standard sub-kilo sizes including the 1 oz line, and coin blanks for sovereign and private mints.

By branded-bar volume Metalor has a quieter retail-bullion presence than PAMP, Argor-Heraeus, or Valcambi, but holds full Good Delivery accreditation and supplies institutional buyers and industrial customers at scale. In 2019 the company announced it would discontinue sourcing gold from artisanal and small-scale mining operations globally — a notable supply-chain due-diligence position that affected how the operation accepts mine-origin material from that point on, and that distinguishes Metalor’s responsible-sourcing posture inside the Swiss refining group.

Why Swiss refining concentrates Good Delivery capacity

The clustering of four LBMA-accredited gold refiners in a single small country — three of them within a thirty-kilometre radius in Ticino — has a structural explanation that builds across post-war Swiss banking, downstream geography, federal regulation, accumulated technical depth, vault and carrier infrastructure, and the responsible-sourcing investment accreditation now requires.

Through the 1960s, 1970s, and 1980s, the major Swiss banks — UBS, Credit Suisse, and Swiss Bank Corporation before its merger into UBS — were among the largest physical bullion dealers in the world, intermediating gold flows between producing countries and consuming markets across Europe, the Middle East, and Asia. That trading volume needed refining capacity in close proximity. Two of the four — Valcambi under Credit Suisse, and Argor under Union Bank of Switzerland — grew up directly inside that bank-led bullion business and were sized for the wholesale flows it generated. Even after the banks divested their refining stakes in the early 2000s (Credit Suisse exiting Valcambi in 2003, UBS exiting Argor at around the same time), the throughput capacity, technical depth, and counterparty network the bank-era buildout had produced stayed in place.

Ticino itself is one reason the cluster sits where it does. The canton borders Italy, with road and rail access into the north of the country and onward to the Mediterranean ports. Italian gold-jewellery manufacturing — the Vicenza and Arezzo districts in particular, historically among the largest gold-fabrication clusters in the world — has long pulled refined bullion southward across that border. Kilobars and grain produced in Mendrisio, Balerna, and Castel San Pietro reach the Italian fabrication centres within hours by road, with the Gotthard route extending the same logistics corridor northward into central Europe.

Federal regulation makes refining a defined economic activity inside Switzerland. The Swiss Precious Metals Control Act sets out hallmark, assay, and trade-license requirements for precious-metals operations on Swiss territory, administered by the Federal Bureau for Precious Metals Control under the Federal Office for Customs and Border Security. Switzerland is one of relatively few jurisdictions where the regulatory framework treats refining as a federally licensed trade with corresponding assay infrastructure: the Federal Bureau operates assay offices at Bern, Le Locle, Chiasso, Zurich, and Geneva that perform official assays on submitted material. For refiners, federal licensing combined with official-assay capability and integrated customs treatment removes friction in cross-border bullion movement.

Time itself matters. Each of the four refiners has been operating on Swiss soil for between sixty and over one-hundred-seventy years — Metalor’s predecessor founded in 1852, Argor in 1951, Valcambi in 1961, PAMP in 1977. Decades of accumulated assay and refining technology, a trained workforce, and a local supplier network of coin-blank tooling and security-packaging firms around the refining sites give the Swiss cluster a depth that newer refining jurisdictions are still catching up with. The Heraeus group’s own refining heritage in Hanau, brought to bear inside Argor-Heraeus, extends that depth into a Germany–Switzerland industrial-precious-metals corridor that exists nowhere else.

Around the refiners sits a dense network of secure vaulting operations. Major bullion vaults at Zurich Airport, in Geneva (the Geneva Free Port), and across customs-bonded warehouses around the country support the international precious-metals carriers — Brink’s, Loomis, Malca-Amit, Ferrari Group, G4S — that move gold between refineries, vaults, and end-buyers globally. The carriers’ Swiss operations, the vault footprint, and the refining capacity reinforce each other: a refiner’s output flows into bonded vaulting and onward to international destinations through carrier infrastructure built around the same flows.

Since the mid-2010s, the practical bar for refiner-level sourcing controls has risen considerably. The OECD Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas (originally published 2011 and expanded since), the LBMA Responsible Gold Guidance, and the Responsible Jewellery Council’s Chain-of-Custody and Code of Practices certifications collectively require substantial investment in audit, traceability, and supplier-onboarding infrastructure inside a refining operation. The established Swiss refiners had the scale and continuity to absorb that investment, and several of them publish annual responsible-sourcing reports under those frameworks. New entrants seeking Good Delivery status today face the compliance burden alongside the technical and financial-standing thresholds, which raises the entry barrier and reinforces the position of the existing Swiss four.

The Swiss refining cluster is the structural outcome of these conditions — banking-era throughput, downstream-market geography, federal licensing, accumulated technical depth, the surrounding vault and carrier network, and the compliance investment the wholesale accreditation system now demands. It is not a tax or secrecy outcome. For a buyer specifying institutional-grade gold today, the Swiss four cover a meaningful share of available refining capacity, alongside the major non-Swiss refiners — Heraeus in Hanau, Rand Refinery in South Africa, Tanaka in Japan, Royal Canadian Mint, Perth Mint, Asahi in Salt Lake City, and the GCC refiners covered in companion articles — that fill out the rest of the LBMA list.

Standards: LBMA Good Delivery and Swiss federal precious-metals control

Two distinct regulatory layers apply to a Swiss-refined gold bar at the same time. Each does different work, sits under a different administering body, and certifies a different thing. A buyer specifying institutional-grade Swiss origin is relying on both.

LBMA Good Delivery. The London Bullion Market Association maintains the Good Delivery list — the global standard for refiner accreditation in the wholesale gold and silver markets. Inclusion on the list is what makes a refiner’s bars deliverable into LBMA-cleared loco-London settlement and, by extension, recognisable across the international wholesale market.

Accreditation under the framework attaches to the refiner. Applicants must clear thresholds on minimum annual refined production, demonstrate financial standing through audited accounts and tangible-net-worth requirements, pass an assay-proficiency test administered by LBMA-appointed referees, and meet the LBMA Responsible Gold Guidance on supply-chain due diligence under the OECD framework. Once accredited, refiners remain under ongoing oversight: the proactive monitoring program reviews accredited refiners on a rolling basis, and each refiner commissions an annual independent assurance audit on its responsible-gold compliance and submits the audit to LBMA. Failure on any of these dimensions results in suspension or removal from the list — a commercial event with substantial consequences for the refiner.

Bar specifications under Good Delivery cover the physical standard. For 400 oz gold bars the requirements include dimensions within a defined range, weight between 350 and 430 troy ounces, fineness of at least 995.0 parts per thousand, and required markings: the refiner’s stamp, serial number, year of manufacture, fineness, and assayer’s mark where the assayer is separate from the refiner. Kilobars and other formats produced by accredited refiners fall outside the strict 400 oz Good Delivery definition while still carrying market recognition through the accredited refiner’s mark.

The full LBMA framework — how the Good Delivery list works, how proactive monitoring runs, the responsible-sourcing audit cycle, and how LBMA accreditation extends to formats below 400 oz — sits in the LBMA Good Delivery explainer. For this article, the relevant point is that all four Swiss refiners hold current LBMA Good Delivery status for gold, with several also holding parallel LPPM (London Platinum and Palladium Market) accreditation for platinum and palladium.

Swiss federal precious-metals control. The Swiss layer rests on the Federal Act on the Control of Trade in Precious Metals and Articles of Precious Metals (Loi sur le contrôle des métaux précieux / Edelmetallkontrollgesetz), originally 1933, and the implementing Ordinance on the Control of Trade in Precious Metals (Ordonnance sur le contrôle des métaux précieux / Edelmetallkontrollverordnung). Administration sits with the Federal Bureau for Precious Metals Control (Bureau central du contrôle des métaux précieux / Zentralamt für Edelmetallkontrolle), part of the Federal Office for Customs and Border Security (formerly the Federal Customs Administration).

Three Bureau functions are relevant to gold-bar supply. Federal trade licensing applies to melters, assayers, and trade assayers operating in Switzerland, and the Swiss refiners hold these licences in their respective categories. Official assay capacity sits at Bureau-operated offices in Bern, Le Locle, Chiasso, Zurich, and Geneva — a Bureau assay carries legal-evidentiary weight, distinct from the refiner’s own internal assay. Import/export control and hallmarking apply to precious-metals goods crossing Swiss borders, and articles of precious metals (jewellery, watch components, and similar) are subject to fineness-mark verification.

For investment-grade gold bars specifically, the Bureau’s role intersects with the refining process and with cross-border movement. Bullion bars carry the refiner’s own marks and assay certification under LBMA Good Delivery rules; the federal hallmark system applies primarily to articles. Bureau supervision still governs the licensing of melters and the operation of refining sites on Swiss territory, and the official-assay capability remains available to support disputes or verification needs.

Together, the two layers cover different ground. Good Delivery certifies the refiner internationally and governs what the bar must physically be in order to clear the wholesale market. The Swiss federal regime governs the refiner’s right to operate inside Switzerland and the movement of metal across Swiss territory. A buyer of Swiss-refined institutional gold leans on the LBMA framework for refiner credibility and bar specification, and on the Swiss federal framework for the operational legitimacy of the refining and trading infrastructure that produced the bar.

Adjacent frameworks sit alongside these and increasingly appear in due-diligence packages. The OECD Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas establishes the international standard for upstream supply-chain due diligence; the LBMA Responsible Gold Guidance is the gold-sector implementation of it for accredited refiners. The Responsible Jewellery Council Chain-of-Custody Standard and Code of Practices certifications are independent third-party schemes that several Swiss refiners hold alongside LBMA accreditation. Together with the Good Delivery framework and the Swiss federal layer, they document the supply-chain controls that institutional and central-bank buyers increasingly require evidence of.

How the four Swiss refiners compare on format orientation

The per-refiner profiles describe what each of the four produces. The comparative view shows where they overlap and where they diverge — what matters when a buyer maps a format requirement to a supplier shortlist.

All four hold Good Delivery accreditation for gold, and all four produce 400 oz Good Delivery cast bars and kilobars. That is the baseline. Below the baseline, format orientation diverges meaningfully — by sub-kilo product depth, by minted-bar branding, by distinctive proprietary formats, and by where each refiner places its commercial weight.

| Format | Argor-Heraeus | Valcambi | PAMP | Metalor |

|---|---|---|---|---|

| 400 oz Good Delivery cast bar | Yes | Yes | Yes | Yes |

| Kilobar — cast | Yes | Yes | Yes | Yes |

| Kilobar — minted | Yes | Yes | Yes | Selected |

| Sub-kilo branded minted bars (1 g–500 g) | Full range | Full range | Full range, deepest line | Standard sizes incl. 1 oz |

| Coin blanks for sovereign and private mints | Yes | Yes | Yes | Yes |

| Semi-finished products and grain | Yes | Yes | Yes | Yes |

| Distinctive proprietary product | Kinebar® | CombiBar (segmentable) | Lady Fortuna, Rosa, FIDES (design series) | — |

| Industrial PM products beyond bullion | Through Heraeus parent | Limited | Limited | Extensive (own portfolio) |

| Branded retail-investment recognition | High | High (CombiBar especially) | Highest among the four | Lower |

A few patterns follow.

At the 400 oz wholesale level the four are interchangeable. A 400 oz cast bar from any of them is, in physical specification and market acceptance, the same Good Delivery instrument. Choice between refiners at this level turns on supply availability and premium structure on the day, not on product differentiation. Standard cast kilobars sit in the same place: an Argor-Heraeus, Valcambi, PAMP, or Metalor cast kilobar trades interchangeably across most institutional secondary-market contexts and is recognised by all major bullion-bank counterparties.

In the minted segment and the sub-kilo formats, refiners diverge. Visible branding, design, and presentation features feed back into retail-investment resale recognition and premium structure. PAMP is the deepest player here and has been since Lady Fortuna’s launch in 1979 — the design’s continuity over more than four decades has carried PAMP-marked minted bars to the highest brand recognition in the segment globally. Argor-Heraeus and Valcambi run extensive sub-kilo minted lines as well; Metalor’s branded retail-investment presence is narrower by comparison. For a buyer whose decision weight sits in retail-investment resale, PAMP is the meaningful differentiator.

Two of the four hold proprietary formats. Valcambi’s CombiBar addresses a divisibility use case that no other Swiss product covers in the same way, and PAMP’s design series — Lady Fortuna, Rosa, and FIDES — occupy the premium end of the minted-bar market on aesthetics and limited-edition cycles. Argor-Heraeus and Metalor offer comparable standard products without comparable proprietary lines.

Industrial-precious-metals overlay differs by group. Argor-Heraeus runs inside the Heraeus parent, which spans automotive-catalyst recycling, semiconductor materials, dental and medical alloys, fibre optics, and electroplating chemistry — refining sits inside that wider group. Metalor’s own group portfolio carries similar industrial scope at the top level. Valcambi and PAMP are more refining-and-bullion-focused as businesses, without comparably broad industrial PM portfolios. For a buyer evaluating supply continuity across cycles, the industrial overlay carries weight: refiners embedded in larger industrial PM groups sit on revenue diversification and technical scale that pure-play bullion refiners do not.

On capacity, Valcambi’s Balerna site sits at the highest single-site refining throughput among the four — publicly cited above 2,000 tonnes of gold annually, built around a high-throughput wholesale model. Argor-Heraeus, PAMP, and Metalor operate at substantial but smaller scale, with proportionally more weight on minted-bar and downstream product alongside wholesale Good Delivery output. Very large institutional volumes — central-bank-scale orders, large 400 oz allocations — make capacity availability a sourcing factor in its own right.

Mapping the picture to a sourcing decision: at the 400 oz wholesale level, all four are technically equivalent and the choice turns on counterparty relationships and availability, with Valcambi’s capacity the most unconstrained. For cast kilobars at institutional scale, again all four are interchangeable across most secondary-market contexts. Where retail-investment resale recognition matters — minted kilobars and sub-kilo branded product — PAMP carries the deepest brand. Segmentable retail-investment formats run through Valcambi’s CombiBar specifically. And for supply continuity rooted in a larger industrial PM group, Argor-Heraeus through the Heraeus parent and Metalor through its own group structure are the two with the deepest industrial overlay.

For institutional buyers focused specifically on the kilobar format, all four Swiss refiners are realistic options at the cast-bar level, with differentiation appearing in minted formats and branded recognition. Format-specific premium structure, secondary-market behaviour, and acquisition mechanics of kilobar transactions sit on the kilobar page itself.

Origin documentation accompanying institutional purchase

A Swiss-refined gold bar acquired through institutional channels arrives with a documentation set establishing its origin, identity, and ownership status. The set itself uses elements common to most institutional gold bars worldwide — what gives Swiss origin its strength is the cleanliness and recognition of each element when the refiner is one of the LBMA-accredited four.

Marks struck or engraved into the bar surface identify the producing refiner directly: Argor-Heraeus’s hallmark, Valcambi’s hallmark, PAMP’s hallmark, or Metalor’s hallmark, each with its own visual signature that the secondary market recognises. Alongside the hallmark, the bar carries a unique serial number, the stated weight, the fineness (typically 999.9 for institutional gold bars from these refiners), the year of manufacture for Good Delivery bars, and the assayer’s mark where the assayer is separate from the refiner. On minted bars the marks appear within the design layout; on cast bars they are stamped into the bar face. Together the marks identify the bar as one specific physical object — which is the foundation everything else builds on.

For minted formats, the assay certificate is integrated with the bar in tamper-evident packaging — the CertiPAMP card for PAMP, equivalent assay cards for Argor-Heraeus and Valcambi minted bars — combining bar and certificate in a single sealed unit. The certificate records the serial number, weight, fineness, and refiner’s assay attestation. Cast kilobars and 400 oz Good Delivery bars travel with a separate assay certificate document, since these formats are designed for vault storage where handheld retail-investment packaging would add little.

When the bar enters allocated storage at an institutional vault — through Brink’s, Loomis, Malca-Amit, or another bullion vault operator — the vault records the bar against the buyer’s allocation by serial number, refiner, weight, and fineness. The allocation record is the documentary instrument that establishes the buyer’s title to a specific physical bar, distinct from a claim against a pool of unallocated metal. The serial number on the bar matches the serial number on the allocation record, and the match is the chain that ties physical identity to ownership title.

Tying that title back to the refinery requires continuous custody documentation. For bars moving through institutional channels from the refiner forward — refiner to bullion bank to end-buyer’s vault, or refiner to authorised distributor to end-buyer’s vault — the carrier documentation, customs records, and vault receipts together form a continuous chain of custody. The chain establishes that the bar has remained inside bonded or vaulted institutional custody from the point it left the refinery, which is the operational basis for treating the bar as primary-market refinery-direct supply.

Secondary-market bars carry a different chain-of-custody picture. The same physical marks remain on the bar, but the chain breaks at each ownership transfer and is reconstructed as the bar passes through dealer or vault hands. Secondary-market Swiss-refined bars from the four still resell at face value across most institutional contexts because the refiner mark is the dominant identification — and the chain documentation is shorter, starting from the most recent custody event rather than from the refinery. For institutional buyers placing weight on continuous chain of custody, refinery-direct primary-market supply remains the cleaner profile.

Detail on how to read refiner marks, verify serial numbers against assay certificates, and inspect a bar physically sits in dedicated articles. At the level of this article, the documentation set enables an institutional buyer of a Swiss-refined bar to establish, at acquisition, the bar’s identity, its origin, its assay status, and its ownership title — each element backed by an entity whose institutional standing is verifiable: the refiner, the assayer, the vault, the carrier. The refining and supply-chain partners that anchor these documents on the supply side — refiners, vault operators, secured carriers — are mapped out at the partners and service providers level.

Sources and references

The facts in this article are drawn from the primary websites of the four refiners, the institutional standards bodies that govern them, and the regulatory authorities under whose framework they operate. The list below groups the sources by what they were used to verify.

The four refiners — primary websites

- Argor-Heraeus SA — argor-heraeus.com

- Valcambi SA — valcambi.com

- PAMP SA / MKS PAMP Group — mkspamp.com, pamp.com

- Metalor Technologies SA — metalor.com

Parent groups and ownership

- Heraeus Precious Metals (parent of Argor-Heraeus) — heraeus-precious-metals.com

- Rajesh Exports Limited (owner of Valcambi) — rajeshindia.com

- Tanaka Kikinzoku Kogyo (owner of Metalor) — tanaka.co.jp

London Bullion Market Association — accreditation, standards, and oversight

- LBMA — lbma.org.uk

- LBMA Good Delivery list (gold) — lbma.org.uk/good-delivery

- LBMA Responsible Gold Guidance and Responsible Sourcing programme — published on the LBMA site under Responsible Sourcing

- LBMA Proactive Monitoring programme — published on the LBMA site under Good Delivery

Swiss federal regulatory framework

- Federal Office for Customs and Border Security (BAZG / OFDF) — bazg.admin.ch

- Central Office for Precious Metals Control / Bureau central du contrôle des métaux précieux — operates within the Federal Office for Customs and Border Security; assay offices in Bern, Le Locle, Chiasso, Zurich, and Geneva

- Federal Act on the Control of Trade in Precious Metals and Articles of Precious Metals (Edelmetallkontrollgesetz / Loi sur le contrôle des métaux précieux), SR 941.31 — fedlex.admin.ch

- Ordinance on the Control of Trade in Precious Metals (Edelmetallkontrollverordnung / Ordonnance sur le contrôle des métaux précieux), SR 941.311 — fedlex.admin.ch

International due-diligence standards

- OECD Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas, including Supplement on Gold — oecd.org

- Responsible Jewellery Council — responsiblejewellery.com

- LPPM (London Platinum and Palladium Market) — lppm.com

Industry and historical context

- Reuters and Financial Times reporting (2003 — Credit Suisse divestment of Valcambi; 2015 — Rajesh Exports acquisition of Valcambi; 2016 — Tanaka Kikinzoku acquisition of Metalor; 2017 — Heraeus consolidation of full ownership of Argor-Heraeus)

- World Gold Council — gold.org — for industry-level gold-supply data

- Reports from the Federal Office for Customs and Border Security on precious-metals control activity in Switzerland

Capacity figures, founding dates, ownership history, and product-range descriptions in this article are drawn from the refiners’ own published materials and the regulatory documents listed above. Where industry reporting was used for ownership-transition dates, the underlying corporate transactions are also recorded on the refiners’ own corporate-history pages.